|

| COVID-19 Update | April 4, 2020 |

View Email in Browser |

|

Yesterday morning on a call with Secretary of the Treasury Steven Mnuchin I received the following updates: 1) If you have a direct deposit on file with the IRS from your 2019 or 2018 taxes, you should receive your one-time tax rebate directly in your account in the next two weeks. 2) If you do not have direct deposit information on file, to receive your one-time tax rebate, you will need to input your information at an IRS portal, which will go live in the coming weeks. 3) If you do not have a bank account, you will likely receive a payment in the mail with your one-time tax rebate. Here are answers to some of the most common questions about how the CARES Act will impact individuals: What are the details of the tax rebate? This comes in the form of a one-time tax rebate check of $1,200 per individual / $2,400 per couple and $500 per child for those with a valid Social Security number. There are no earned income or tax liability requirements to receive these rebate checks. The full rebate amount is available for those with incomes at or below $75,000 for individuals, $112,500 for head of household, and $150,000 for married couples. Individuals making more than these thresholds will receive a reduced rebate check. This income threshold will be calculated by using your 2018 or 2019 taxes, whichever you have filed most recently. Arkansans that haven’t filed taxes in 2018 or 2019 but who have a valid Social Security number are still eligible, but the check won’t come automatically. There will be a process to contact the IRS to receive your check. What are the changes to retirement accounts? The CARES Act loosens rules on retirement accounts. Older Americans that are subject to mandatory required minimum distributions (RMD) from their retirement accounts, and have not already done so, would be able to keep their capital invested instead of being forced to cash out to draw on that capital without penalty, which would be suspended for 2020. Similarly, the bill also waives the ten percent penalty on coronavirus-related early distributions from 401(k)s and IRAs, which applies to distributions made at any time during 2020. What if you’ve lost your job due to COVID-19? Arkansas provides unemployment benefits for a maximum of 16 weeks. The CARES Act adds up to $600 dollars per week to your benefits for up to four months and extends the time you can receive benefits by 13 weeks. These benefits will expire on July 31, 2020. Unemployment benefits also have been enhanced to cover more workers including self-employed and independent contractors, like gig workers and Uber drivers, who do not usually qualify for unemployment. Overall, the CARES Act provides $250 billion in funding for the expansion of unemployment benefits, the largest increase ever. Have any benefits in the Supplemental Nutrition Assistance Program (SNAP) been expanded? At the state level, Governor Hutchison has suspended work requirements for SNAP recipients at least through the end of April. The state is also expediting applications to help families access benefits faster. At the federal level, the U.S. Department of Agriculture’s (USDA) Food and Nutrition Service (FNS) has expanded SNAP eligibility to families with children who would have received free or reduced lunch if in school. Additional measures include: allotting emergency supplements to states for the distribution of monthly SNAP benefits up to the maximum for eligible families; suspending the time limit on benefits for able-bodied adults without dependents; and waiving the physical presence requirement for applying for and receiving benefits under WIC (Special Supplemental Nutrition Program for Women, Infants, and Children). Do you still have to pay your student loans? The Trump Administration already ended interest accrual on federal student loans through September 30, 2020. The CARES Act paused monthly repayment requirements forfederal student loans for six months with no penalty. The interest accrual stoppage is automatic, but students must contact the Department of Education to pause their payments. Federal student loan borrowers also will lose no time towards loan forgiveness programs, such as the Public Service Loan Forgiveness program. In addition, a great new benefit of the CARES Act is that employers can now contribute $5,250 per year to help their employees pay off their federal student loans, which will not be taxed for the employee. Is there any relief on paying your mortgage? The CARES Act prohibits foreclosures on any federally backed mortgages for 60-days, allows borrowers affected by COVID-19 to shift any missed payments to the end of their mortgage, with no added penalties or interest, for 180 days, halts evictions for renters in properties with federally-backed mortgages for 120 days, and gives relief to multifamily property owners through forbearance on any federally backed mortgage.

On Wednesday, I spoke with David Sanders, the Director of Innovate Arkansas, part of Winrock International, about programs available to small- and medium-sized businesses during the ongoing public health and economic crisis. We discussed how the Coronavirus Aid, Relief, and Economic Security (CARES) Act and the Paycheck Protection Program provide capital to struggling businesses and economic relief to gig workers and independent operators. To watch the full interview, click HERE or on the image below.

Here are answers to some of the most common questions that people have regarding how the CARES Act will impact businesses in Arkansas: The United States Treasury’s Paycheck Protection Program went live yesterday. It authorizes up to $349 billion toward job retention and other expenses for the millions of Americans employed by small businesses. Small businesses and eligible nonprofit organizations, veterans’ organizations, and Tribal businesses described in the Small Business Act, as well as individuals who are self-employed or are independent contractors, are eligible if they also meet program size standards. See the links below for more information from Treasury's website:

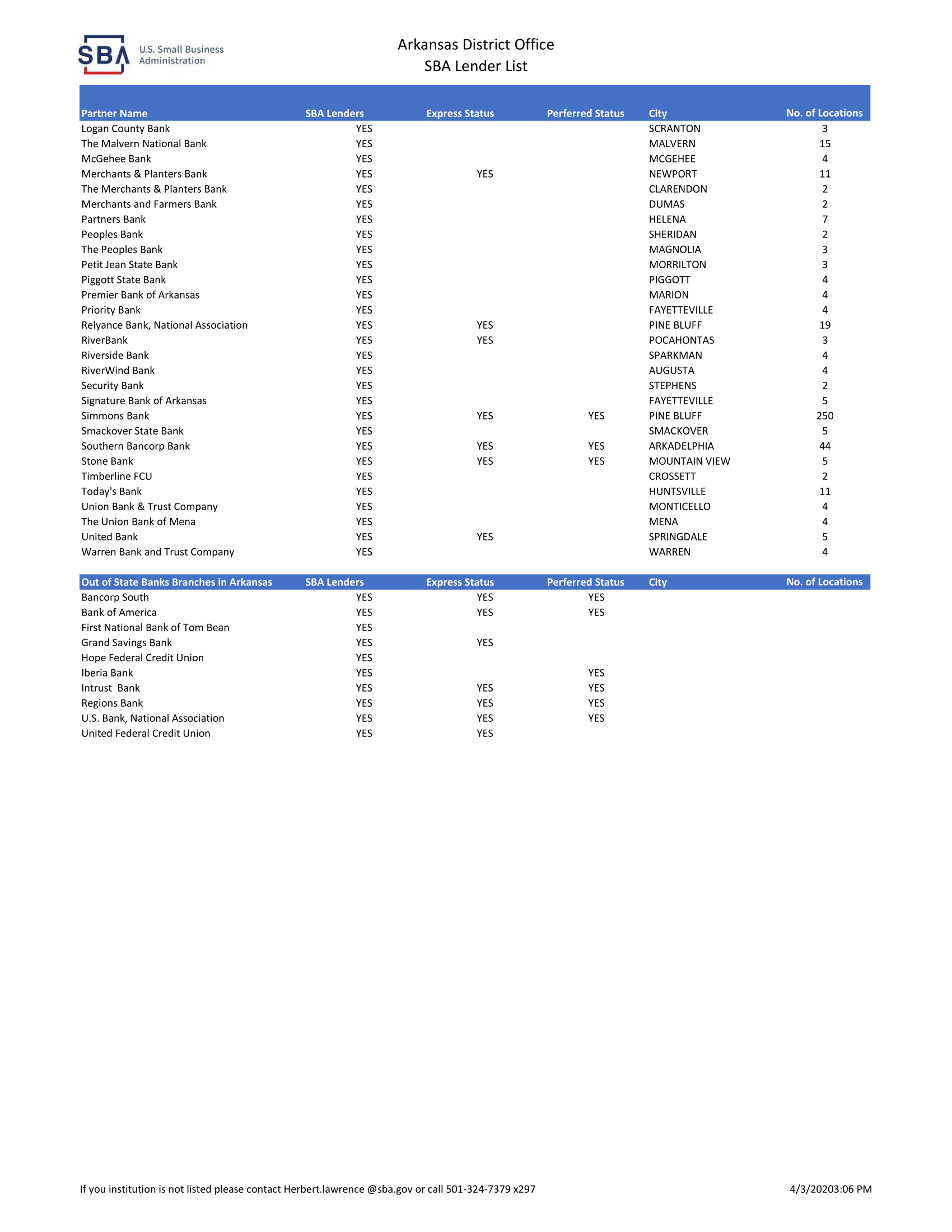

Who is eligible for the loan? You are eligible for a loan if you are a small business that employs 500 employees or fewer, or if your business is in an industry that has an employee-based size standard through Small Business Administration (SBA) that is higher than 500 employees. In addition, if you are a restaurant, hotel, or business that falls within the North American Industry Classification System (NAICS) code 72, “Accommodation and Food Services,” and each of your locations has 500 employees or fewer, you are eligible. Tribal businesses, 501(c)(19) veteran organizations, and 501(c)(3) nonprofits, including religious organizations, will be eligible for the program. Nonprofit organizations are subject to SBA’s affiliation standards. Independently owned franchises with under 500 employees, who are approved by SBA, are also eligible. Eligible franchises can be found through SBA’s Franchise Directory. I am an independent contractor or gig economy worker; am I eligible? Yes. Sole proprietors, independent contractors, gig economy workers, and self-employed individuals are all eligible for the Paycheck Protection Program. What is the maximum amount I can borrow? The amount any small business is eligible to borrow is 250 percent of their average monthly payroll expenses, up to a total of $10 million. This amount is intended to cover eight weeks of payroll expenses and any additional amounts for making payments towards debt obligations. This eight-week period may be applied to any time frame between February 15, 2020, and June 30, 2020. Seasonal business expenses will be measured using a 12-week period beginning February 15, 2019, or March 1, 2019, whichever the seasonal employer chooses. What is the covered period of the loan? The covered period during which expenses can be forgiven extends from February 15, 2020, to June 30, 2020. Borrowers can choose which eight weeks they want to count towards the covered period, which can start as early as February 15, 2020. How can I use the money such that the loan will be forgiven? The amount of principal that may be forgiven is equal to the sum of expenses for payroll, existing interest payments on mortgages, rent payments, leases, and utility service agreements. Payroll costs include employee salaries (up to an annual rate of pay of $100,000), hourly wages and cash tips, paid sick or medical leave, and group health insurance premiums. If you would like to use the Paycheck Protection Program for other business-related expenses, like inventory, you can, but that portion of the loan will not be forgiven. When is the loan forgiven? The loan is forgiven at the end of the eight-week period after you take out the loan. Borrowers will work with lenders to verify covered expenses and the proper amount of forgiveness. How much of my loan will be forgiven? The purpose of the Paycheck Protection Program is to help you retain your employees, at their current base pay. If you keep all of your employees, the entirety of the loan will be forgiven. You will owe money when your loan is due if you use the loan amount for anything other than payroll costs, mortgage interest, rent, and utilities payments over the eight weeks after getting the loan. Not more than 25% of the forgiven amount may be for non-payroll costs. You will also owe money if you do not maintain your staff and payroll. Am I responsible for interest on the forgiven loan amount? No, if the full principal of the Paycheck Protection Program loan is forgiven, the borrower is not responsible for the interest accrued in the eight-week covered period. The remainder of the loan that is not forgiven will operate according to the loan terms agreed upon by you and the lender. What are the interest rate and terms for the loan amount that is not forgiven? The interest rate of the loan will be 1.0%, and the maturity of the loan will be two years. You will not have to pay any fees on the loan, and collateral requirements and personal guarantees are waived. Loan payments will be deferred for six months following the date of disbursement of the loan. When is the application deadline for the Paycheck Protection Program? Applicants are eligible to apply for the Paycheck Protection Program loan until June 30, 2020. I took out a bridge loan through my state; am I eligible to apply for the Paycheck Protection Program? Yes, you can take out a state bridge loan and still be eligible for the Paycheck Protection Program loan. What is the Employee Retention Credit? The CARES Act creates a refundable payroll related tax credit that is designed to help businesses, or eligible employers, keep employees on the payroll when COVID-19 forces the business to suspend or close its operations. The tax credit is equal to 50% of wages and compensation. There is an overall limit on wages per employee of $10,000. The credit is provided through December 31, 2020. Employers are eligible if they have been fully or partially suspended as a result of a government order, or if they experience a 50 percent reduction in quarterly receipts as a result of the crisis. For employers with 100 or fewer full-time employees, they may claim a credit for wages paid to all of their employees, up to $10,000 a person. For employers with more than 100 employees, they may claim a credit for those employees who are furloughed or face reduced hours as a result of the employer’s closure or economic hardship. This tax credit is not available if the employer takes an SBA paycheck protection loan. If I have applied for, or received an Economic Injury Disaster Loan (EIDL) related to COVID-19 before the Paycheck Protection Program became available, will I be able to refinance into a Paycheck Protection Program loan? Yes. If you received an EIDL loan related to COVID-19 between January 31, 2020 and April 3, 2020, you can apply for a Paycheck Protection Loan. If your EIDL loan was not used for payroll costs, it does not affect your eligibility for a Paycheck Protection Program loan. If you EIDL loan was used for payroll costs, your Paycheck Protection Program loan must be used to refinance your EIDL loan. Proceeds from any advance up to $10,000 on the EIDL loan will be deducted from the loan forgiveness amount on your Paycheck Protection Program loan. Which banks in Arkansas are ready to provide Paycheck Protection Program loans? The chart below outlines the current Small Business Administration (SBA) lenders in Arkansas. The ones under the preferred status are current preferred 7(a) lenders with the SBA and have the authority to provide PPP loans. Other banks should be granted authority in the near term.

I have more questions; where can I get answers? My staff and I are here to serve you. Contact me at (501) 324-5941 or at french.hill@mail.house.gov. We will get you the information you need. It is an honor to serve as your Congressman. Sincerely,  Representative French Hill |

|

| Office Locations | |||

|

|||

|

|

| UPDATE SUBSCRIPTION OPTIONS | PRIVACY POLICY | CONTACT US |